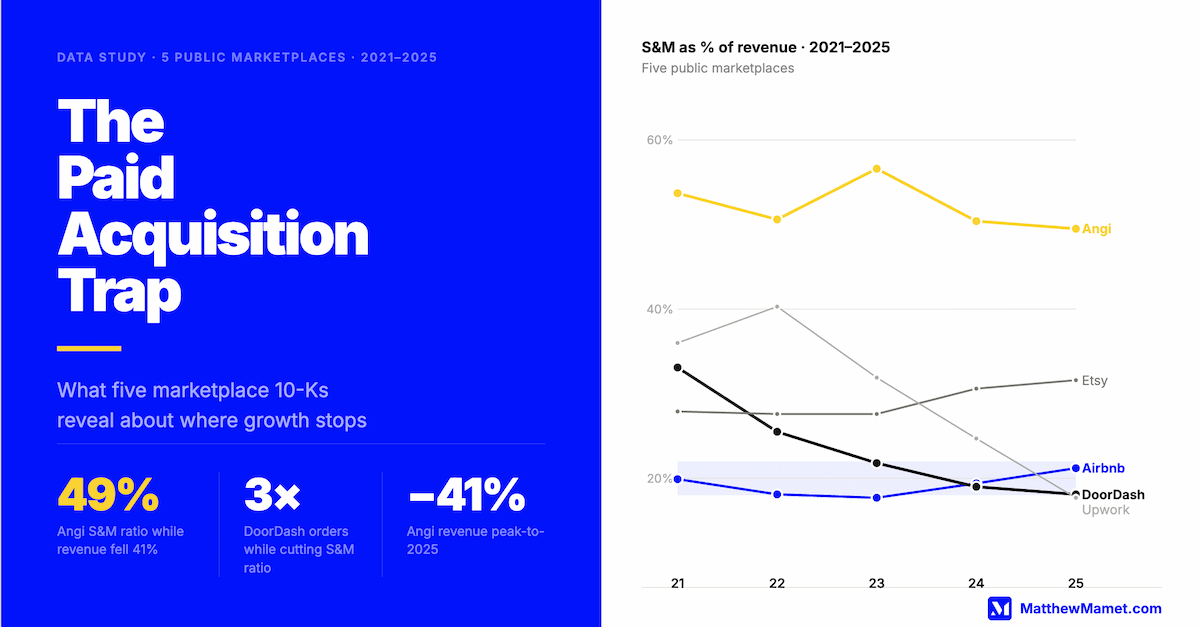

Marketplace businesses have been built for thirty years on a single assumption: consumers need help comparing options. The comparison step, research, evaluate, decide, is hard enough and consequential enough that a platform can insert itself between the consumer and the outcome and charge for the privilege.

That assumption is being tested at scale for the first time.

AI agents don't compare options and return results for a human to evaluate. They take the goal as input, do the research, form a recommendation, and either present a single answer or execute the transaction. The comparison step doesn't disappear. It moves from the consumer to the agent, and the agent has no reason to route through a marketplace whose only value was organizing the comparison.

The following data comes from three marketplace categories. In each case, the evidence is behavioral, measured in search volume, and financial, measured in revenue and subscriber data from public earnings reports. The pattern across all three is consistent enough to treat as a structural shift rather than category-specific noise.

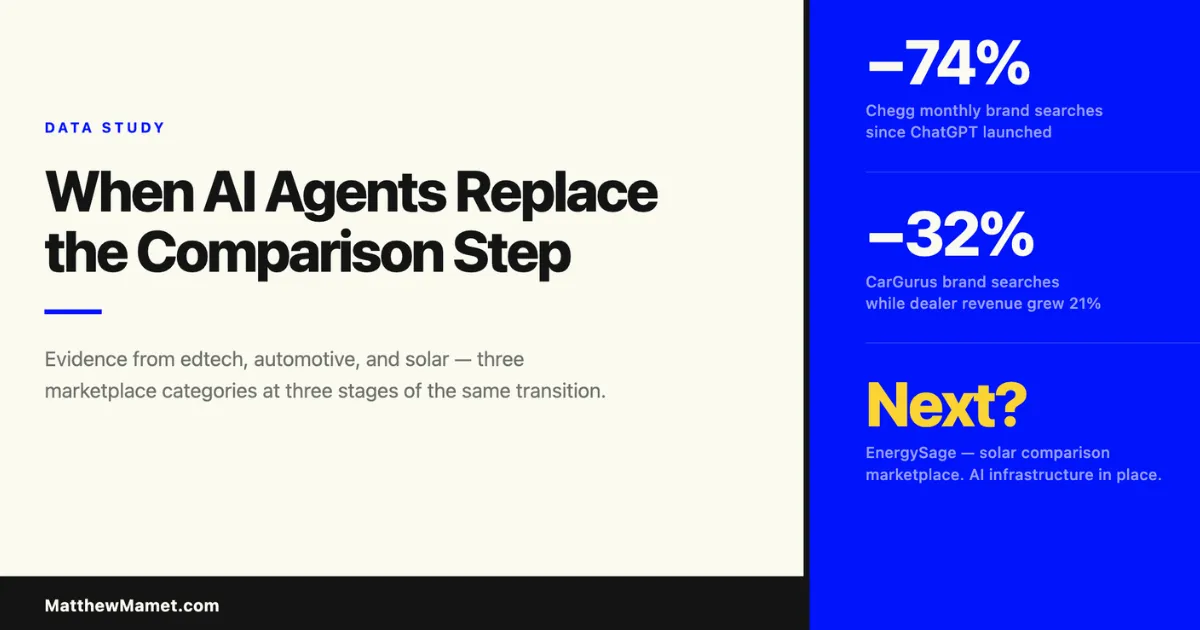

Edtech: The First Market to Break

The edtech case is the clearest because the mechanism is documented by the company itself.

Chegg built a marketplace for academic help. Students searched for solutions to specific problems: textbook questions, homework assignments, exam prep. Chegg organized those solutions and charged $19.95 per month for access. The model required students to search, find, and extract. The comparison step was built into the product design.

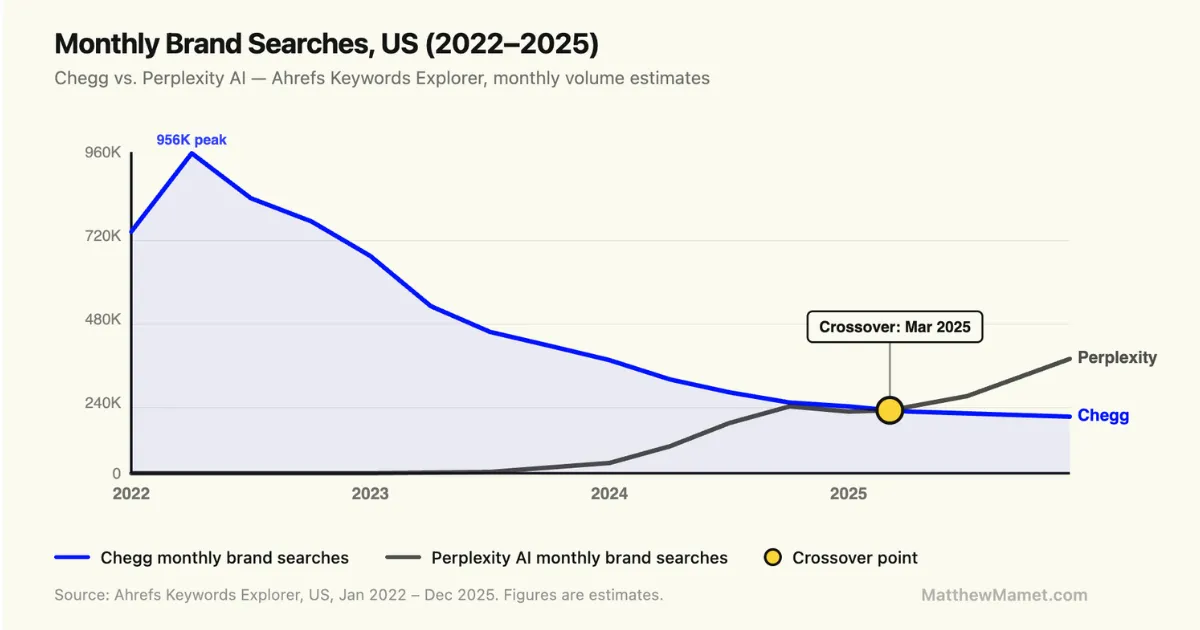

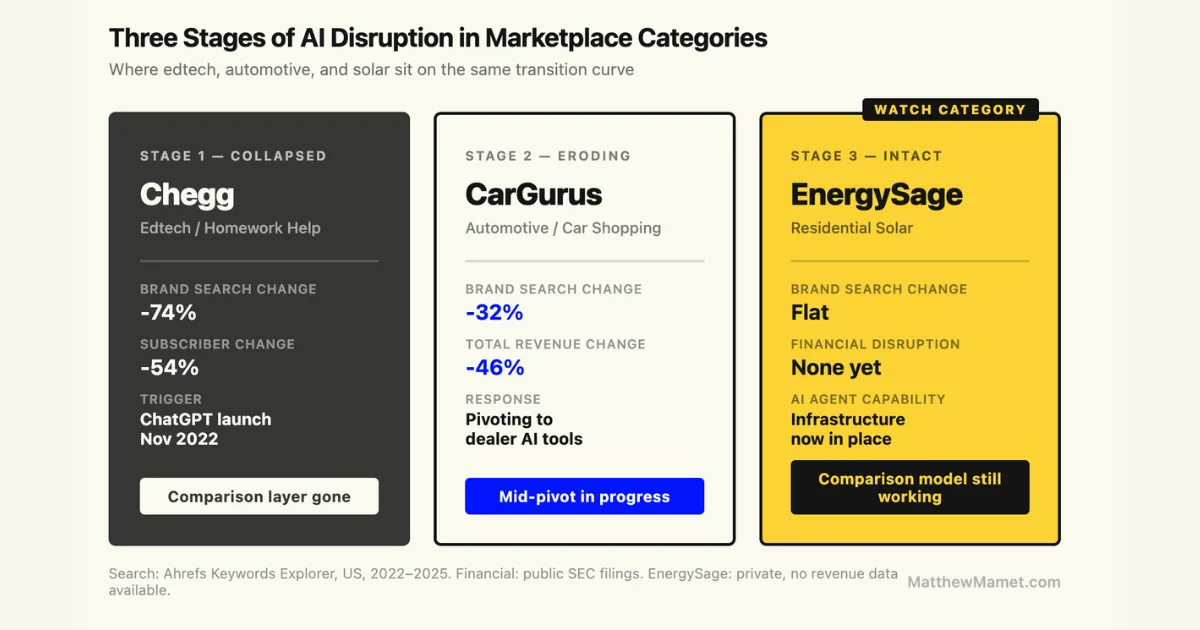

At peak in early 2022, consumers were searching for "Chegg" roughly 956,000 times per month in the United States. The business had 7.8 million paying subscribers. Revenue was growing at 29% year-over-year.

ChatGPT launched in November 2022. The mechanism of disruption was immediate and direct: a student who previously searched Chegg for a solution could describe the problem to an AI and receive the answer directly. No search. No comparison. No subscription required. The agent absorbed the step Chegg was selling access to.

The search data shows what happened to consumer behavior before it showed up in the financials. By the 2023 to 2024 school year, average monthly searches for Chegg had fallen to 405,000, a 44% decline from the 2022 average. In May 2023, Chegg became the first public company to name ChatGPT explicitly as a cause of business deterioration and withdrew its annual guidance. By 2024, the subscriber base had declined to 3.6 million, a 54% drop from peak, and the company posted an $837 million net loss on $617 million in revenue.

The search volume collapse preceded the subscriber collapse by roughly two quarters. Consumers stopped searching before they stopped paying.

The crossover is not a metaphor. It is a measurement of the moment when more consumers were navigating to an AI answer engine than to the comparison marketplace in the same category.

| 2022 | 2025 | Change | |

|---|---|---|---|

| Chegg monthly brand searches (avg) | 721,000 | 187,000 | -74% |

| Chegg subscribers | 7.8M | 3.6M | -54% |

| Chegg annual revenue | ~$740M | $617M | -17% |

| AI homework helper monthly searches (avg) | 5 | 34,600 | +6,900x |

| Perplexity AI monthly searches (avg) | 1,100 | 344,000 | +313x |

Automotive: The Erosion in Progress

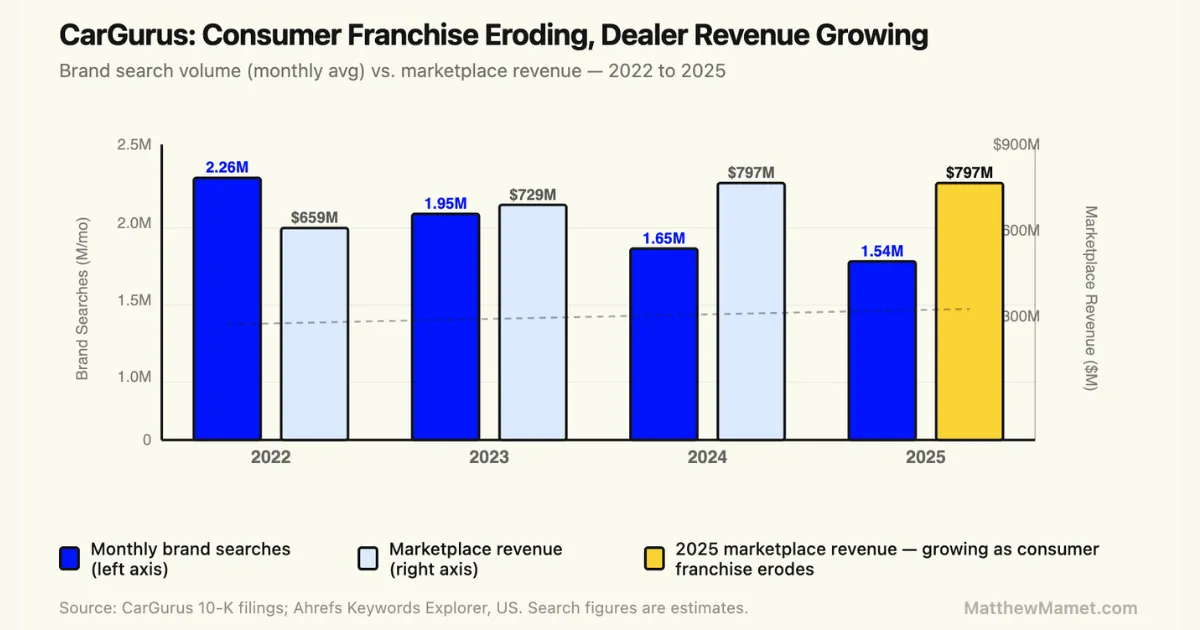

CarGurus was founded in Boston in 2006 and went public in 2017 on a well-executed premise: car buyers were navigating a fragmented, information-asymmetric market, and a platform that aggregated inventory and made pricing transparent would attract both consumer demand and dealer subscription revenue.

The model worked. CarGurus became the most-visited automotive shopping platform in the United States. At peak in early 2022, consumers were searching for "CarGurus" 2.5 million times per month.

The CarGurus story is different from Chegg's because the collapse hasn't happened yet. But the behavioral erosion is visible and accelerating.

Average monthly brand searches declined from 2.26 million in 2022 to 1.54 million in 2025, a 32% decline in three years. By December 2025, monthly searches had fallen 44% from the February 2022 peak. CarGurus' total revenue peaked at $1.655 billion in 2022 and has declined since, settling at $894 million in 2024, a 46% drop that was partly operational but structurally signals a business under pressure.

The more telling number is what CarGurus is doing in response. In 2024 and 2025, CarGurus has been explicitly repositioning from a consumer-facing comparison platform to a dealer-facing AI intelligence platform. Their CEO described it in their Q4 2024 earnings call as moving from being a "marketplace" to being a "growth solutions partner" for dealers. They launched Dealer Data Insights, Next Best Deal Rating, and Acquisition Insights, tools that use AI to help dealers price, acquire, and sell inventory. In Q4 2024, nearly one million pricing changes were made based on AI recommendations. Premium dealer tier migration was up 23% year-over-year.

CarGurus is actively trying to escape the comparison layer. That strategic pivot is itself the evidence. The company with the deepest consumer-facing automotive comparison business in the United States is betting its future on selling AI tools to dealers, because they understand that the consumer comparison step is the part of their business most exposed to AI agents.

| 2022 | 2025 | Change | |

|---|---|---|---|

| CarGurus monthly brand searches (avg) | 2.26M | 1.54M | -32% |

| CarGurus total revenue | $1.655B | $894M | -46% |

| CarGurus marketplace revenue | $659M | $797M | +21% |

| CarGurus strategic direction | Consumer comparison | Dealer AI tools | Pivot in progress |

The marketplace revenue growth alongside total revenue decline and brand search decline is the tell: CarGurus is extracting more value per dealer relationship even as the consumer comparison franchise erodes. That is what a business in mid-pivot looks like.

Solar: The Category That Hasn't Broken ...Yet

EnergySage is the leading residential solar comparison marketplace in the United States. It was founded in Boston in 2009, acquired by Schneider Electric in 2022, and operates on a model nearly identical to CarGurus: a homeowner submits a request, multiple installers submit standardized quotes, and the consumer compares and selects.

EnergySage brand search volume has been essentially flat from 2022 through 2025, ranging between 5,000 and 12,000 monthly searches with no clear trend in either direction. There is no financial disruption yet. The model is working despite recent headwinds in the solar industry brought about by unfriendly regulatory decisions at the Federal and State (California) level.

But the category has structural characteristics that make it a strong candidate for the same transition that has already hit edtech and is underway in automotive.

A residential solar decision involves the same complexity profile that made comparison marketplaces successful in other categories: multiple vendors, inconsistent pricing, technical specifications the consumer cannot easily evaluate, and a significant financial commitment with long payback periods. EnergySage's value proposition is nearly identical to Chegg's at the category level: it organizes the comparison step for a decision the consumer finds difficult to figure out alone.

AI agents are already handling this type of decision in adjacent categories. A consumer asking an AI agent "should I get solar, and if so which installer in my area" is describing exactly the query the comparison marketplace was built to answer. The agent can pull permit data, utility rates, equipment pricing, installer reviews, and financing options and return a recommendation without the consumer ever visiting a comparison platform. EnergySage released an AI-enabled solar instant quoting feature in 2024. The infrastructure to do this exists today.

The search volume data suggests the transition has started. EnergySage brand search is declining. But the category is watching two upstream indicators, residential solar installation rates and AI agent adoption for home improvement decisions, that will determine when the comparison layer becomes the bottleneck rather than the enabler.

| Metric | 2022 | 2025 | Change |

|---|---|---|---|

| EnergySage monthly brand searches (avg) | 8,000 | 6,700 | -18% change |

| Residential solar category status | Comparison model working | Comparison model working | No change yet |

| AI agent capability for solar decisions | Not available | Available | Infrastructure in place |

What the Pattern Says

The three cases represent three stages of the same transition: one category where the comparison layer has already collapsed, one where it is visibly eroding with the incumbent mid-pivot, and one where the structural conditions are in place but the disruption hasn't started.

The mechanism is the same in each case. The comparison marketplace organized information so consumers could evaluate options. The AI agent evaluates options directly and returns a recommendation. The consumer doesn't stop needing the decision made. They stop needing to make it themselves.

What survives the transition is not the comparison layer. It is the fulfillment layer: the physical installer, the vehicle on the lot, the tutoring session with a human. The comparison marketplace that owns only the research and selection step has no fulfillment moat. The one that also owns the transaction, the installation, the logistics, or the ongoing service relationship has something an AI agent can direct but cannot replace.

Methodology: Financial data for Chegg and CarGurus sourced from public SEC 10-K filings and quarterly earnings releases. Search volume data sourced from Ahrefs Keywords Explorer historical monthly volume, US only, January 2022 through December 2025. EnergySage is a private subsidiary of Schneider Electric; no revenue data is publicly available. All search volume figures are estimates.